- Share on Facebook4

- Share on Pinterest

- Share on Twitter

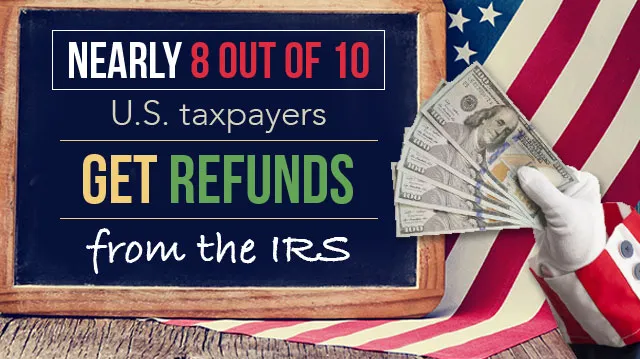

For eight out of 10 US taxpayers, tax season is synonymous with refund season. According to an H&R Block analysis of 2012 refund data, 84 percent of households earning $50,000 or less will see a refund. That percentage drops to 62 percent for households earning between $100,000 and $200,000 and 34 percent for those earning over $200,000. In a way, everyone wins. In another way, only the government has won.

Over the course of a lifetime, the average American will pay $250,000 in interest — certainly money they could have used for retirement instead. Interest is dead financial weight, just extra cash shelled out for the privilege of borrowing money for big-ticket items such as cars, homes and an education. Credit cards, too. Any money overpaid in taxes is money that could have been spent paying debt and lessening the interest burden of a given household.

This is especially relevant to those Americans who use their refund to pay off debt, as over 40 percent have planned to do each year since 2007. Of course, what we plan to do and what we actually do doesn’t always line up. CNN Money reports that last year Americans were most likely instead to pay current bills or finance a vacation or car with their refund.

If the plan is to purchase something, overpaying the government through your taxes becomes a relatively effective saving mechanism. It may not be returned with interest, but it does build up over the year and is returned to you in a useful lump sum.

Moreover, not all tax refund money has been overpaid. A good portion of this refund is due to the mysterious inner-workings of the tax code. The Earned Income Tax Credit increases refunds to low-income individuals, especially those with children. Qualifying individuals might see a refund larger than taxes withheld. Other people might earn tax deductions for qualifying childcare expenses, educational costs or interest paid on a home mortgage. In short, it pays to understand our convoluted tax system.

Moreover, not all tax refund money has been overpaid. A good portion of this refund is due to the mysterious inner-workings of the tax code. The Earned Income Tax Credit increases refunds to low-income individuals, especially those with children. Qualifying individuals might see a refund larger than taxes withheld. Other people might earn tax deductions for qualifying childcare expenses, educational costs or interest paid on a home mortgage. In short, it pays to understand our convoluted tax system.

Whether this year’s refund was an overpayment rectified or one borne out of credits and deductions, a tax refund can be used to bolster savings, pay off debt or invest in your future. The mismatch between Americans’ intentions and actual spending habits is usually a result of poor financial planning. One-third of Americans don’t have a financial plan at all, while over half know they should have a better plan.

There is no one-size-fits-all financial plan. Likewise, there is no universally applicable recommendation for how to spend a sizable chunk of cash. People prioritizing building good credit probably want to pay down their credit cards to 30 percent of each card’s limit. Those interested in minimizing interest payments would be better off paying their high-interest debts first. Others might prioritize financial stability and choose to bolster their savings before speeding up debt repayment. Still others might have their finances in order well enough to spend $5,000 on that dream vacation to Tahiti.

In every scenario, however, having a financial plan and sticking to it is a good idea. What better time to go over your finances and sort out priorities for the upcoming year than right when that tax refund arrives in your account.

—Erin Wildermuth

Erin is a freelance writer, photographer and filmmaker. She is passionate about moving beyond party politics to identify pragmatic solutions to social, economic and political problems. Her writing has appeared in the Washington Times, the American Spectator, Doublethink and Scuba Diver Magazine. She spends her free time scuba diving, snowboarding and ravenously reading popular nonfiction. Erin holds a master’s degree in International Political Economy from the London School of Economics.

Sources:

http://money.cnn.com/2015/01/13/pf/taxes/taxpayer-refunds/index.html

http://nypost.com/2015/01/15/the-average-american-pays-280k-in-interest

http://money.cnn.com/pf/storysupplement/tax_refunds

http://time.com/money/3733393/tax-refunds-debt

https://turbotax.intuit.com/tax-tools/tax-tips/Tax-Deductions-and-Credits/5-Facts-About-the-Earned-Income-Tax-Credit/INF18089.html

http://www.cnbc.com/2015/04/29/one-third-of-americans-lack-a-future-financial-plan-study.html

- Share on Facebook4

- Share on Pinterest

- Share on Twitter